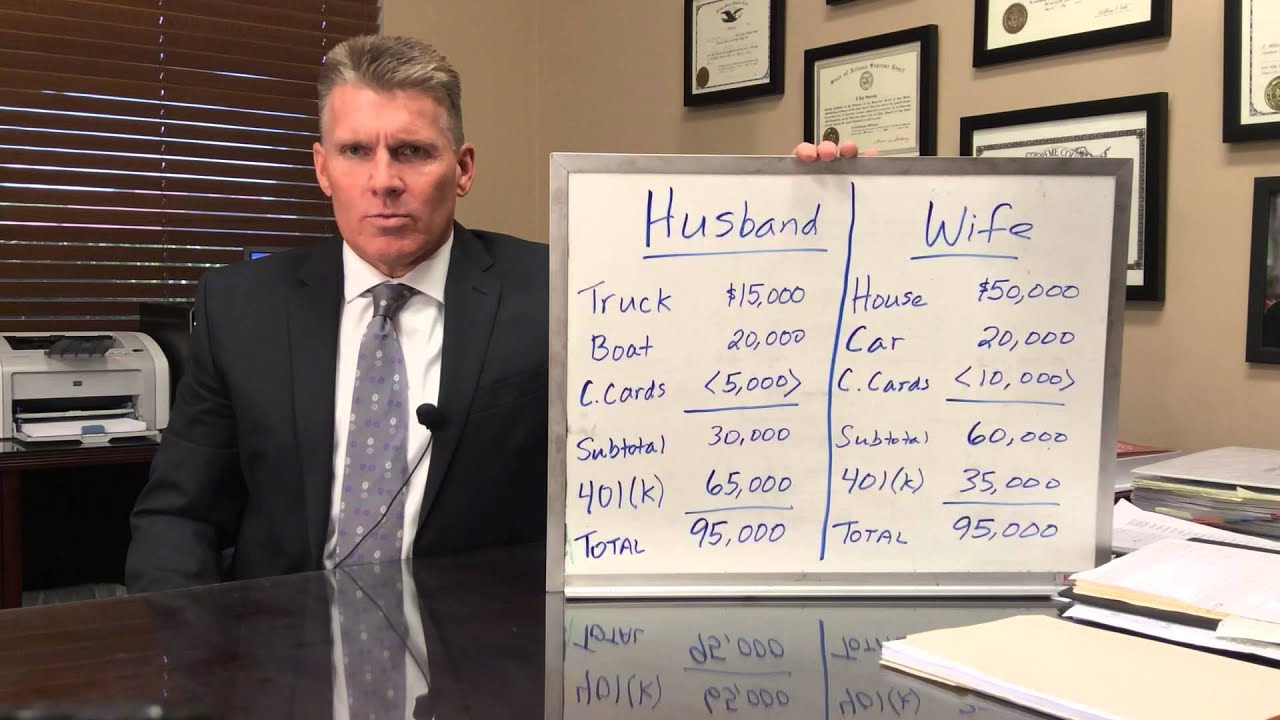

Divorce Division of Assets Illustrated In a previous post, I addressed the process of identifying, categorizing and valuing assets prior to the assets’ being divided in an Arizona divorce case. This post will provide an example of how assets and debts could be divided in a hypothetical case. Under A.R.S. §25-318, a judge in an Arizona divorce case is to divide assets equitably, “though not necessarily in kind . . . .” This phrase–“not necessarily in kind”–simply means that, while the overall division of assets and debts must be fair, or substantially equal, an Arizona judge is not required to equally divide each individual asset equally. Similarly, the judge is not required to liquidate all assets and divide the proceeds equally. In the example I will use, the husband and wife have community property consisting of a house with $50,000 equity, a truck with $15,000 equity, a car with $20,000 equity, a boat worth $20,000, a 401(k) worth $100,000, and credit cards totaling $15,000. The table below illustrates one possible division of these assets and debts so that, at the “bottom line”, each party receives $95,000 net. HUSBAND WIFE Truck/Debt $15,000 House/Mortgage $50,000 Boat 20,000 Car/Debt 20,000 401(k) 65,000 401(k) 35,000 Credit Cards (5000) Credit Cards (10,000) Total $95,000 Total $95,000 Note in this example that none of the assets needs to be liquidated. As long as the “bottom line” is equitable, or substantially equal, the division of the marital assets is valid under the law. The example assumes, of course, that there is no premarital agreement dictating a division of assets other than that prescribed by Arizona community property law. Furthermore, although our example ignores tax consequences for simplicity’s sake, in the real world, the 401(k) dollars would need to be tax-effected before the division is calculated in order to achieve a truly “equitable” division of the assets. Copyright © 2017 by Scoresby Family Law – J. Kyle Scoresby, P.C. All rights reserved....(read more)

LEARN MORE ABOUT: IRA Accounts

CONVERTING IRA TO GOLD: Gold IRA Account

CONVERTING IRA TO SILVER: Silver IRA Account

REVEALED: Best Gold Backed IRA

Divorce can be a challenging and emotionally draining process, and one of the most significant aspects of a divorce is the division of assets. When couples get married, they often accumulate assets together, and when they get divorced, they must divide those assets. This process is called the division of assets, and it can be complicated depending on the individual situations of each couple. In the United States, there are two ways to divide assets in a divorce: equitable distribution and community property. Equitable distribution is the most common method, and it involves dividing the assets in a fair and just manner. Under this method, the court will consider several factors when dividing the assets, including the length of the marriage, the income and earning potential of each spouse, and the contributions of each spouse to the marriage. Community property, on the other hand, is a method used in some states that considers all assets acquired during the marriage to be joint property. In community property states, assets are divided equally between the two parties. Regardless of the method used, the division of assets can be a complex process, and it often requires the assistance of legal professionals. To illustrate how assets are divided in a divorce, let's look at an example. John and Jane have been married for ten years, and during that time, they have accumulated several assets together, including a house, two cars, a joint bank account, and individual retirement accounts (IRAs). When they decide to get a divorce, they must divide these assets between them. Under the equitable distribution method, the court will consider several factors when dividing these assets. First, they will look at the length of the marriage. In this case, John and Jane have been married for ten years, which is a significant amount of time. The court will also consider the income and earning potential of each spouse. In this case, John earns more than Jane, and he has a higher earning potential. The court will also examine the contributions of each spouse to the marriage. In this case, both John and Jane contributed to the marriage equally. After examining these factors, the court will make a decision on how to divide the assets. They may decide to award the house to Jane since she will have primary custody of their children, and they may award John more of the retirement accounts since he has a higher earning potential. Both the joint bank account and the cars may be split evenly between the two parties. In community property states, the process would be different. In this case, all of the assets would be split equally between John and Jane, regardless of the factors involved. In conclusion, the division of assets in a divorce can be a complicated process, and it often requires the assistance of legal professionals. The equitable distribution method is the most common method used in the United States, and it involves dividing assets fairly and justly. Community property is another method used in some states, and it dictates that all assets acquired during the marriage are joint property and should be divided equally between both parties. Ultimately, the division of assets will depend on the individual circumstances of each couple. https://inflationprotection.org/illustrating-the-division-of-assets-in-divorce-a-comprehensive-guide/?feed_id=91834&_unique_id=644a0eae37902 #Inflation #Retirement #GoldIRA #Wealth #Investing #401k #A.R.S.Section25318 #ArizonaJudge #assetsdonthavetobeliquidated #car #communitypropertyonly #creditcards #debt #fairandequitabledivision #house #mortgage #notnecessarily5050 #notnecessarilyinkind #premaritalagreementconsidered #substantiallyequal #taxconsequencesconsidered #SpousalIRA #401k #A.R.S.Section25318 #ArizonaJudge #assetsdonthavetobeliquidated #car #communitypropertyonly #creditcards #debt #fairandequitabledivision #house #mortgage #notnecessarily5050 #notnecessarilyinkind #premaritalagreementconsidered #substantiallyequal #taxconsequencesconsidered

Comments

Post a Comment