Have you ever wondered what the difference is between an IRA and a Roth IRA? Don't worry this question is more common than you might think and we're here to help. Check out all of our videos and become a financial champion....(read more)

Have you ever wondered what the difference is between an IRA and a Roth IRA? Don't worry this question is more common than you might think and we're here to help. Check out all of our videos and become a financial champion....(read more)

LEARN MORE ABOUT: IRA Accounts INVESTING IN A GOLD IRA: Gold IRA Account INVESTING IN A SILVER IRA: Silver IRA Account REVEALED: Best Gold Backed IRA

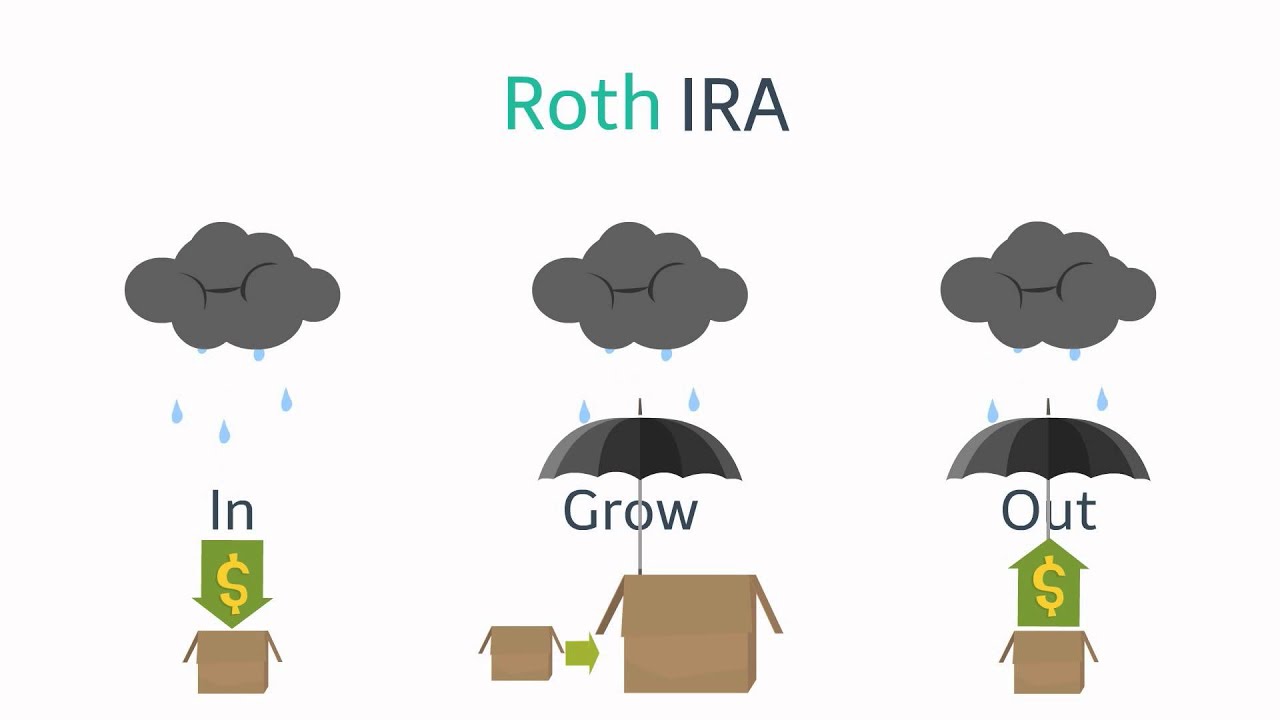

Roth vs Traditional IRA: Choosing the Right retirement account Planning for retirement is a significant financial goal that everyone should consider. One of the key decisions to make when saving for retirement is choosing between a Roth IRA and a Traditional IRA. Understanding the differences between these two types of individual retirement accounts (IRAs) is crucial in determining which option best suits your needs and financial situation. 1. Taxation The primary distinguishing factor between Roth and Traditional IRAs is their tax treatment. With a Traditional IRA, contributions are typically tax-deductible, reducing your taxable income for the year in which contributions are made. However, withdrawals made during retirement are taxed as ordinary income. On the other hand, Roth IRA contributions are made with after-tax dollars, meaning the money you contribute has already been taxed. The advantage here is that you won't owe any taxes when you withdraw funds during retirement. Additionally, qualified distributions from a Roth IRA are tax-free, as long as certain conditions are met. 2. Income and Age Eligibility Another important factor to consider is eligibility. With a Traditional IRA, anyone with earned income can contribute, and there is no age limit for contributions. However, once you reach the age of 72, you must begin taking Required Minimum Distributions (RMDs) from your Traditional IRA. In contrast, Roth IRAs have income limits that determine eligibility. As of 2021, individuals with a modified adjusted gross income (MAGI) above $140,000, and married couples filing jointly with a MAGI above $208,000, are not eligible to contribute. However, if your income falls within these limits, you can contribute to a Roth IRA regardless of your age. 3. Withdrawal Rules It's important to consider the withdrawal rules when choosing between a Traditional and Roth IRA. Traditional IRA distributions are subject to income tax in retirement and, if withdrawals are made before the age of 59 ½, an additional 10% early withdrawal penalty may also apply. Roth IRA contributions can be withdrawn at any time without tax or penalty, as these funds have already been taxed. Additionally, after a Roth IRA has been open for at least five years and the account holder is aged 59 ½ or older, qualified distributions of both contributions and earnings can be withdrawn tax and penalty-free. 4. Estate Planning When it comes to estate planning, the type of IRA you choose can have different implications. With a Traditional IRA, beneficiaries who inherit the account will be subject to income tax on any distributions they receive. In contrast, Roth IRA beneficiaries can inherit the account income-tax-free, provided the account holder has had the Roth IRA for at least five years. In conclusion, the choice between a Roth and Traditional IRA ultimately depends on your specific circumstances and goals. If you expect to be in a lower tax bracket during retirement or want to maximize tax-free withdrawals, a Roth IRA may be more suitable. On the other hand, if you prefer the immediate tax benefits of deductions and are comfortable with taxable withdrawals in retirement, a Traditional IRA may be the better option. It's always advisable to consult with a financial advisor who can analyze your individual situation and guide you towards the most appropriate retirement account. Remember, planning for retirement is a long-term commitment that requires careful consideration and regular review to ensure financial security in the future. https://inflationprotection.org/comparison-between-roth-and-traditional-iras/?feed_id=133484&_unique_id=64f8af5af3337 #Inflation #Retirement #GoldIRA #Wealth #Investing #FinanceIndustry #individualretirementaccount #PersonalFinanceTVGenre #RetirementQuotationSubject #RetirementPlanningLiteratureSubject #RothIRA #traditionalIRA #TraditionalIRA #FinanceIndustry #individualretirementaccount #PersonalFinanceTVGenre #RetirementQuotationSubject #RetirementPlanningLiteratureSubject #RothIRA #traditionalIRA

Comments

Post a Comment